Through July 29th, the US Market (Russell 3000 Index) is up 8.64%! Not only that, but most major asset classes have had strong starts to the year.

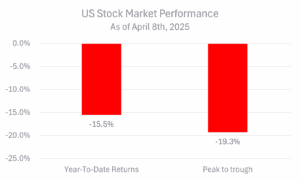

This might be shocking to you, considering a little over 3 months ago on April 8th, the US Market was DOWN 15.5%, and in the middle of a -19.31% drawdown from all-time highs.

If you were a client at that time, you likely heard us reiterating that your portfolio is built for moments like this. Diversification is your friend. Market drawdowns are normal and expected. And most importantly, staying in your seat and trusting your investment plan is key.

With US markets now recovering and up over 8% for the year, this is a great moment to revisit some of those key principles, the data that supports them, and how they held up during this most recent drawdown:

Lesson #1: Drawdowns Should Be Expected

Perhaps the most important mindset shift for investors is to expect market crashes and drawdowns, they’re part of the deal.

Stock prices reflect investor expectations about future earnings and risk. When those expectations shift, whether from a global pandemic like in 2020 or broad-based tariffs like we saw this year, stock prices can change quickly and dramatically. That doesn’t mean the market is broken or this time is different. It means the market is doing what it’s supposed to do: react to new information.

So, can we – or anyone – accurately predict when these events will happen? No.

But do we expect them as investors and build for them in financial plans? Absolutely.

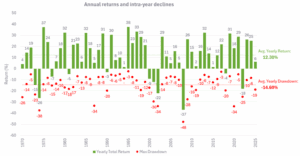

Historically, going back to 1926, U.S. stocks have had negative returns in more than 25% of calendar years. But even more common are intra-year drawdowns that markets experience. Since 1970, the U.S. market has delivered average annual returns of around 12% – but with an average annual drawdown EACH YEAR of -14.6%. In fact, in 21 out of the past 56 years, the market saw a 15%+ decline – that’s about once every 2.7 years.

When you zoom out, you see that these drawdowns are temporary and are part of the journey. Markets have shown their resilience over time.

Lesson #2: Diversification Matters

Diversification and how your structure your portfolio is crucial to driving successful long-term outcomes. Periods of volatility often highlight the importance of having diversifiers in your portfolio.

This chart shows the year-to-date relative performance of various asset classes versus U.S. stocks as of April 8th, meaning how much each asset class outperformed or underperformed US stocks when they were at their lowest point.

For example: International stocks had outperformed the U.S. by over 13%, and U.S. bonds outperformed U.S. stocks by more than 17%.

Even though U.S. markets have since recovered, that diversification played a key role in softening the drawdown for investors. For those making withdrawals at the time, it also provided flexibility to access parts of the portfolio that weren’t as heavily impacted. Helping to avoid needing to sell US stocks at the bottom to fund a distribution.

So, while headlines focused on U.S. market declines and specific stocks, diversified portfolios, like those we build at Greenspring, told a very different story.

Lesson #3: Emotional Decisions Can Derail Long-Term Success

The decisions you make during periods of volatility can have a lasting impact on your financial success.

Let’s go back to April 8th, markets were at their lowest point of the drawdown. Imagine two investors:

– Investor A ignored the headlines, went for a walk, stayed invested and is up +8.64% year-to-date (as of 7/29/25).

– Investor B panicked, sold out of the market, and then regretted it – buying back in the very next day after the market rebounded over 9% on April 9th. Their return? -0.82%

Investor B missed just one day, but it was the best day of the year. That one day made a meaningful difference in returns compared to Investor A, who did nothing.

History shows that the best and worst market days tend to be clustered. Timing your exit is hard. Timing your re-entry is even harder. And the odds of missing the worst days while still catching the best ones? Extremely low. Mistiming just a few days can have a major impact on long-term outcomes.

So, What Can You Do Now?

With markets back in positive territory, but the memory of the drawdown still fresh – now is a great time to pause and reflect:

-

- How did you feel during the drawdown earlier this year?

- Did the volatility make you overly anxious or cause you to lose sleep? If so, it might be time to explore a more conservative allocation if it still helps you reach your goals.

- On the flip side, if you felt confident – or even excited to invest more – you may be in a position to take on additional risk.

Either way, this is a great opportunity to reconnect with your advisor. Let’s revisit how your financial plan is built to weather different environments and ensure it aligns with both your goals and your comfort with risk.

The Bottom Line

Drawdowns are a normal part of investing. And while we know that intellectually, they still feel unsettling in the moment – especially as they are typically accompanied by scary headlines, uncertainty, or major global events.

What matters most isn’t trying to avoid them. It’s having a plan for them, responding thoughtfully, and designing portfolios that can hold up through difficult times.

History continues to show that patient, disciplined investors – who stay diversified and stick to their plan – are rewarded over time.

If you’d like to review your portfolio, revisit your plan, or talk through your investment strategy – we’re here to help.